Major US indices failed to retain its initial gains in the aftermath of the US June jobs report last week, with a mid-day sell-off on relative high volume forcing an eventual close in the red (DJIA -0.55%; S&P 500 -0.29%; Nasdaq -0.13%). The takeaway from the job report was a downside surprise in US job additions (209,000 versus 225,000 forecast) and some persistence in wage growth (4.4% versus 4.2% forecast), which largely validated market rate expectations of having one last 25 basis-point (bp) rate hike at the upcoming Fed meeting to conclude the overall hiking cycle.

A softer read in labour market conditions reflects some degree of policy success thus far, with private payrolls rising by just 149,000, way below the 200,000 consensus. Nevertheless, more progress still needs to be seen with unemployment rate reversing lower to 3.6% (from previous 3.7%) and average weekly hours ticking slightly higher to 34.4 versus previous 34.3, overall anchoring views for the Fed to keep a high-for-longer rate outlook in place. Over the past month, there has been a pushback in rate-cut timeline, with current market pricing pointing to May next year as the turning point.

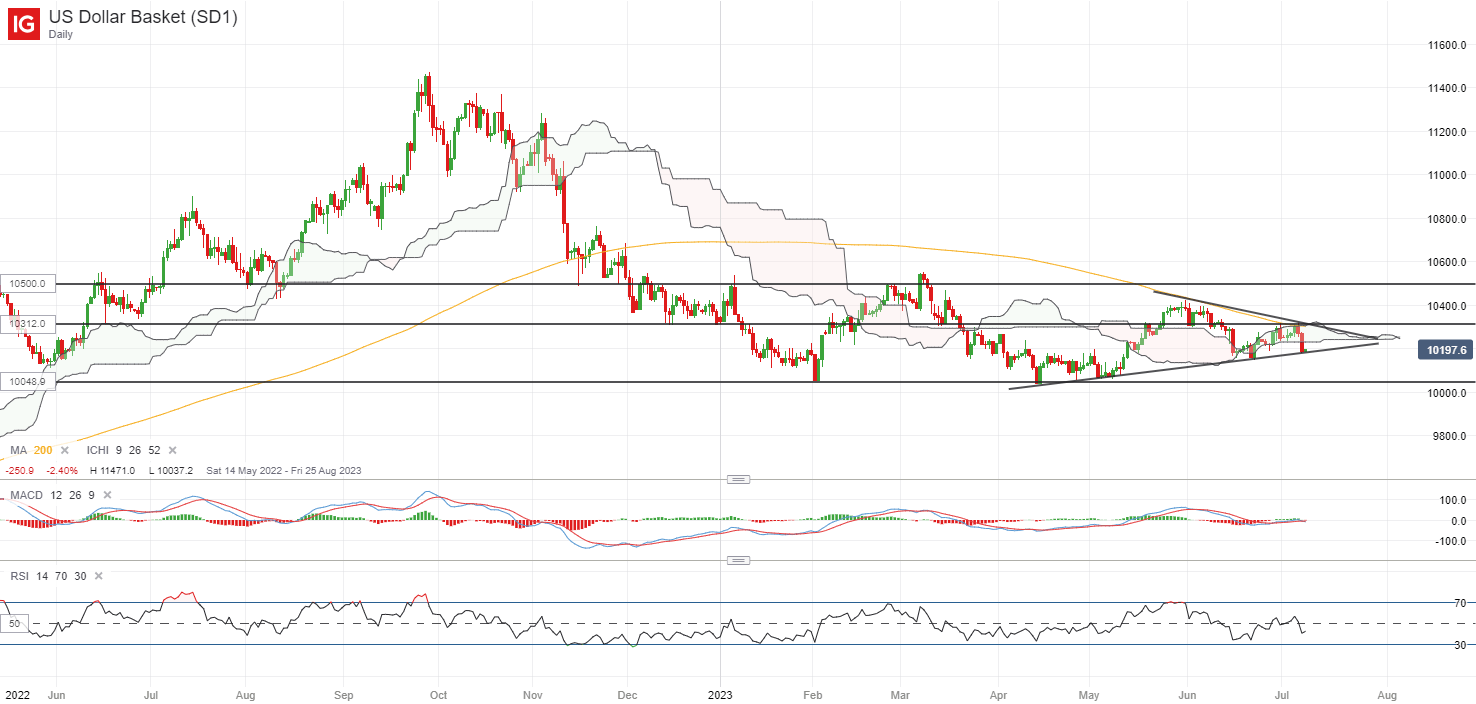

The two-year Treasury yields ended lower by 3.5 bp, while the 10-year yields defended its 4% level with its fourth straight day of gains. The US dollar did not take the weaker-than-expected US job report too well, with a 0.8% plunge in its aftermath. This follows after a retest of its 103.12 level of resistance, which failed to find a successful upward break since June 2023. For now, an upward trendline may serve as near-term support, with any failure to hold potentially leaving the year-to-date low at the 100.50 level on watch. A series of Fedspeak will be lined up today, with any fresh views around the recent US job report in focus.

Source: IG charts

Asia Open

Asian stocks look set for a slight positive start, with Nikkei +0.30%, ASX +0.37% and KOSPI +0.12% at the time of writing. Treasury Secretary Janet Yellen’s visit to China seems to lay the ground for more communication ahead, but any significant thawing in US-China relations remains to be seen, especially with recent export controls in place. At least for now, the meeting seems to conclude on a warmer tone with the intention for cooperation.

Ahead, China’s inflation figures will be in focus. Soft domestic demand thus far have forced consumer prices to rise on average by just 0.3% over the past three months, with another close-to-zero reading likely to echo recent calls for more to be done by Chinese authorities in the second half of this year. Expectations are for another subdued reading of 0.2% year-on-year, unchanged from May, while producer prices are expected to contract further to 5% from previous 4.6%.

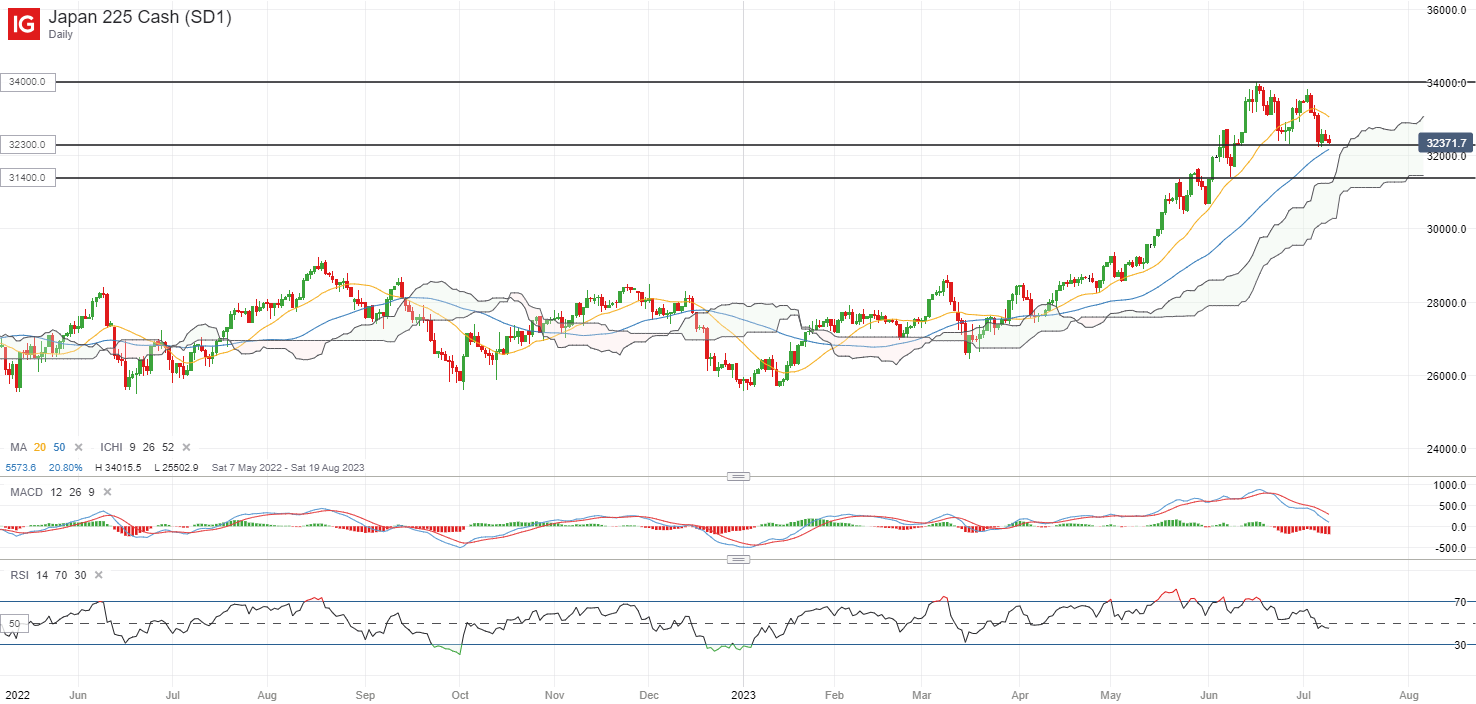

Following a 32% rally since the start of the year, the Nikkei has recently formed a double-top pattern, as lower highs on Relative Strength Index (RSI) and declining moving average convergence/divergence (MACD) point to some moderating upward momentum. The 32,300 level will be the crucial neckline to hold, where some dip-buying was sighted back in June this year. Failure to defend the 32,300 level may confirm the bearish formation, which may leave the 31,400 level on watch, followed by the 30,600 level (projection of double-top breakdown).

Source: IG charts

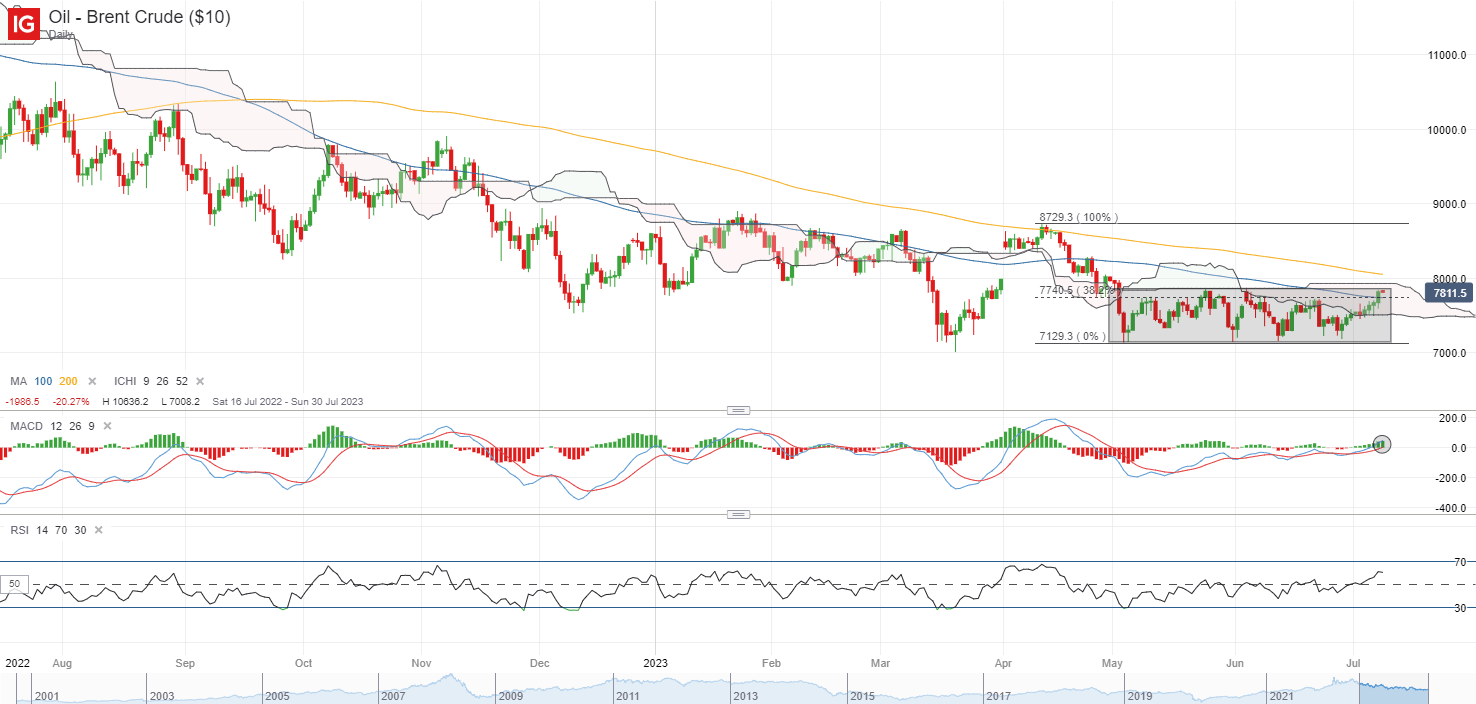

On the watchlist: Brent crude prices attempting for a break above near-term range

After being locked within a near-term consolidation pattern since May this year, Brent crude prices are back to retest the upper edge of the range last week, as tighter-supply conditions from Saudi Arabia and Russia’s production cuts and a weaker US dollar provides the catalysts for some dip-buying. Hopes for some recovery in the second half of this year may be pinned on expectations for China to bring in more stimulus in the months ahead while US economic conditions retain some resilience.

On the technical front, the MACD has crossed above the zero level for the first time in two months, with a similar move in the RSI above its key 50 level, which signals buyers taking over some control with increasing positive momentum. Near-term, a cross above the US$80.00 level may be on watch to provide the conviction for a move to retest its year-to-date high at the US$88.62 level.

Source: IG charts

Friday: DJIA -0.55%; S&P 500 -0.29%; Nasdaq -0.13%, DAX +0.48%, FTSE -0.32%