The US dollar is likely to drift lower, driven by softer economic data which appears to be paving the way for a rate cut later this year. However, a strong economy means the US public may have to wait longer than other developed countries before it can start to lower interest rates. Over the next three months, the dollar is expected to ease but the journey is likely to be choppy due to a robust inflation outlook from the Fed whereby it anticipates only reaching the 2% target in 2026.

Growth, Inflation, and the Labour Market – A Real Mixed Bag

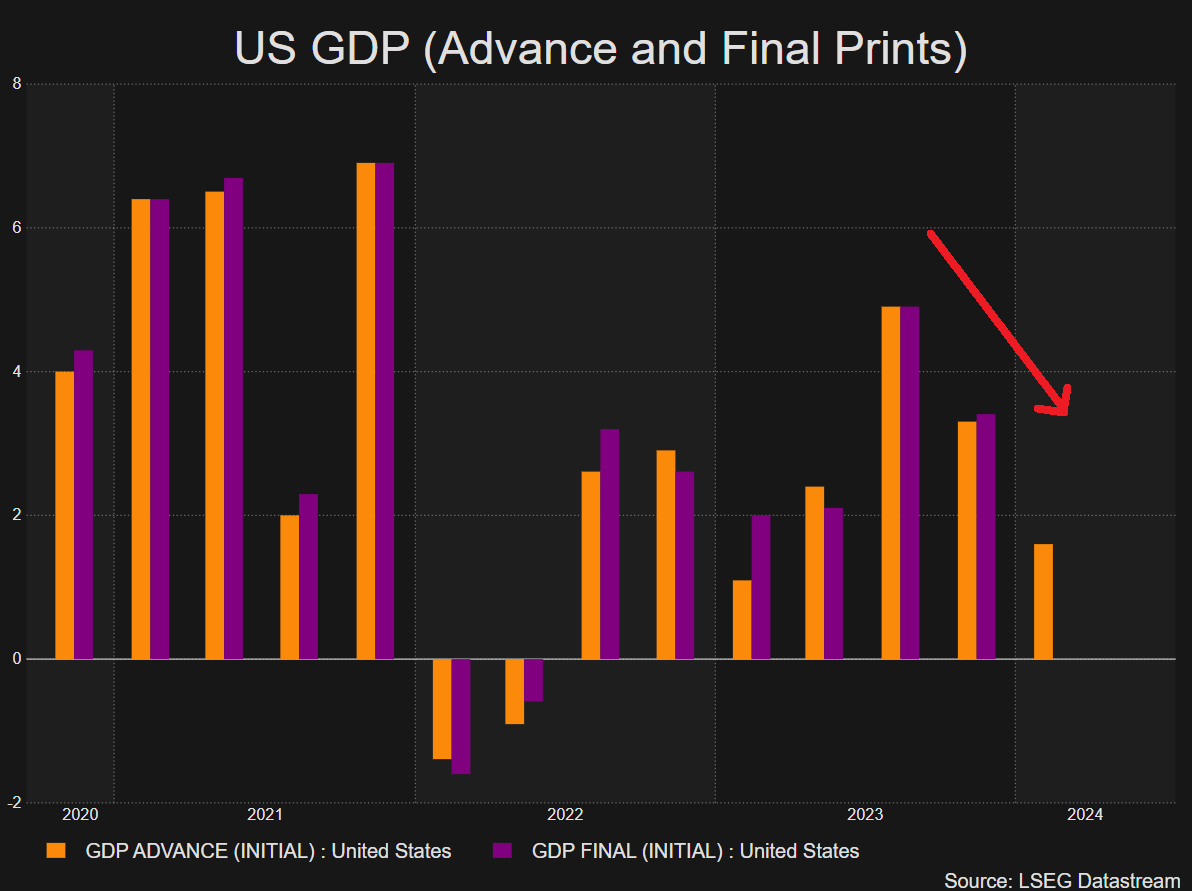

Economic growth is moderating but still robust, disinflation is back on track, and the job market shows small signs of easing despite a massive NFP beat in May. The Fed is hopeful that the strong labour market will usher in a soft landing when it does eventually decide to cut rates with Q3 potentially marking the start of the rate cutting cycle if the data allows (September). Should growth deteriorate alongside the continued progress in inflation, US shorter-term yields have room to fall further and could weigh on the dollar. One risk to the lower growth trend appears via the Atlanta Fed’s GDPNow forecast which suggests Q2 GDP is on track to bounce back to 3% (as of June 20th).

US GDP Growth (Quarter-on-Quarter)

Source: Refinitiv, prepared by Richard Snow

US Inflation Back on the Right Path

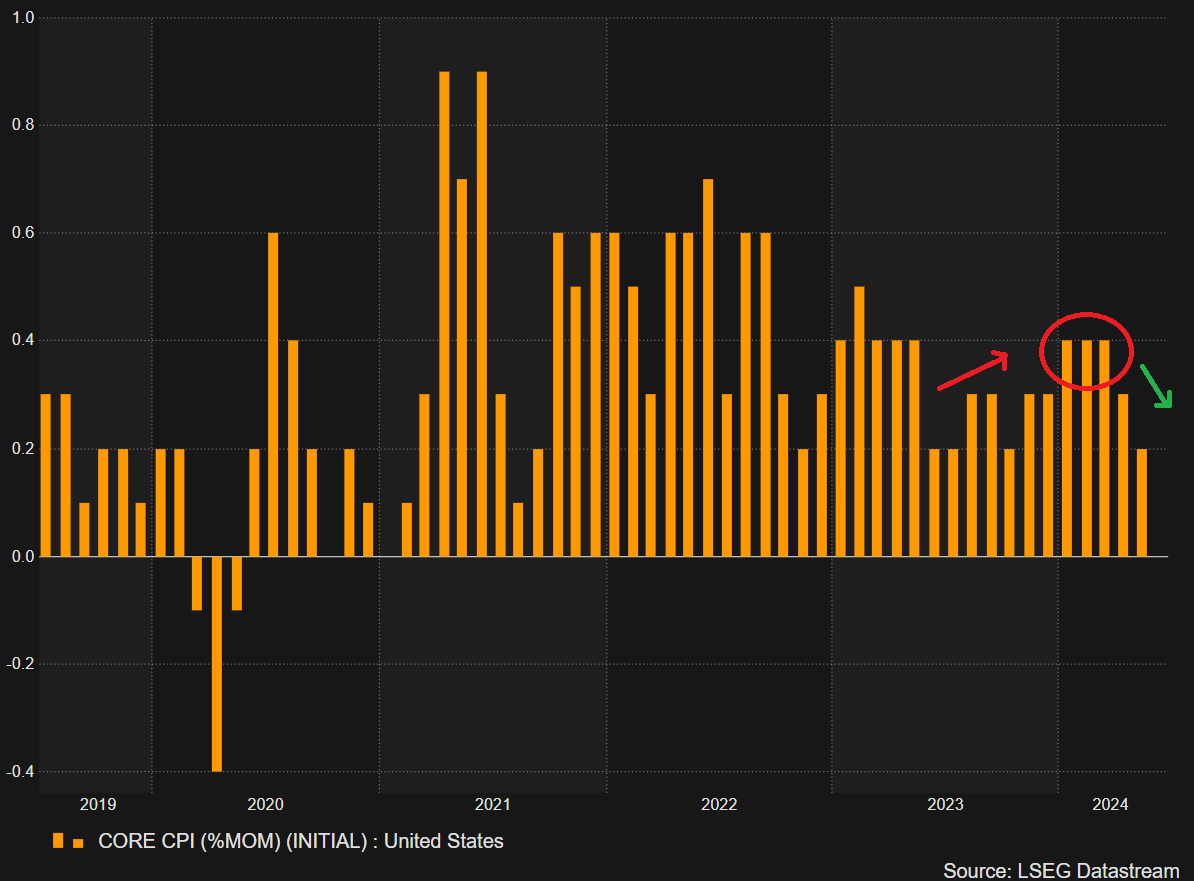

At the centre of the data will be inflation which declined in the first half of the year despite a spate of troubling core CPI prints (month-on-month) that weighed on Fed officials’ confidence of reaching 2% in a timeous manner. Thanks to improved data in April and May, the Fed will likely look for more encouraging signs in the coming months in the hope to build the necessary confidence to finally cut interest rates once or even twice this year.

US Core CPI (Month-on-Month)

Source: Refinitiv, prepared by Richard Snow

After acquiring a thorough understanding of the fundamentals impacting the US dollar in Q3, why not see what the technical setup suggests by downloading the full US dollar forecast for the third quarter?

Recommended by Richard Snow

Get Your Free USD Forecast

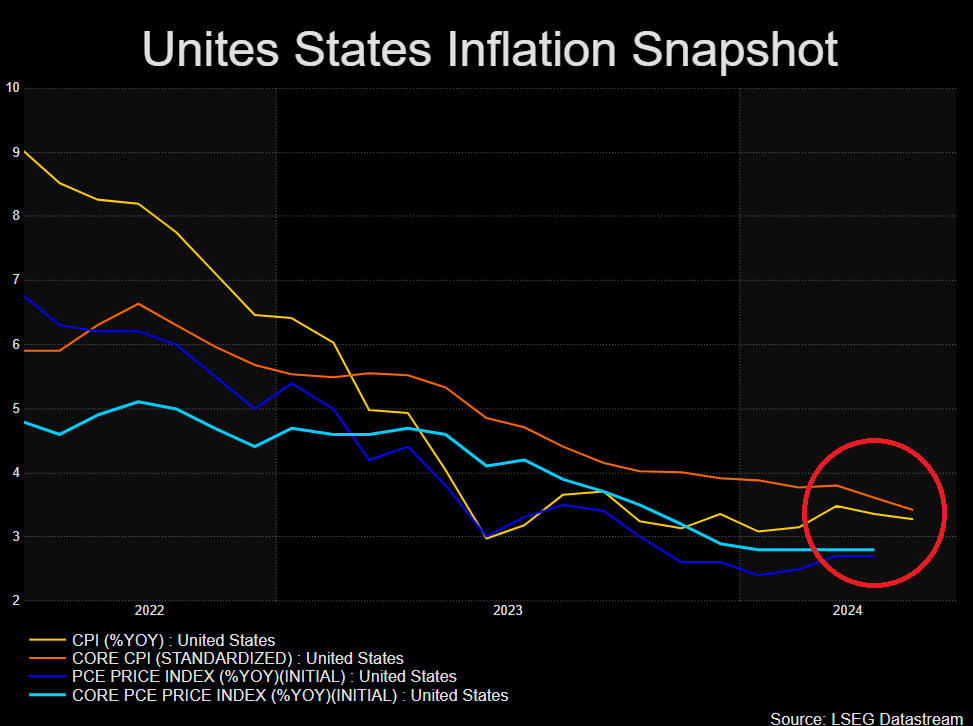

Headline and core measures of both CPI and PCE versions of inflation are heading lower. At the time of writing the US PCE data for May has not yet been released but it is expected to be contained, much like the CPI data. As such, markets may start to fully price in two rate cuts in 2024 which is likely to weigh on the greenback. Services inflation remains a blemish on an otherwise positive scorecard for the Fed and could keep the dollar supported in the absence of any meaningful declines in the reading.

US Inflation Continues Lower

Source: Refinitiv, prepared by Richard Snow

US Labour Market Shows Signs of Easing

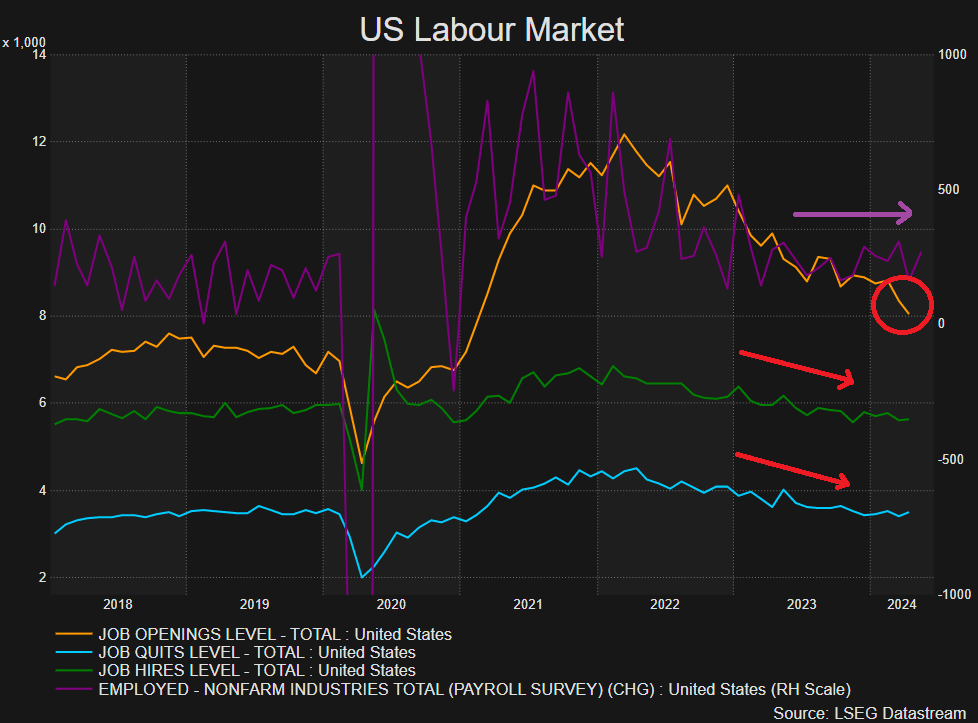

The labour market has shown signs of easing via downward trending job openings, job hires and job quits but progress has been limited. NFP data revealed another shock to the upside as more people found jobs in May than originally anticipated. However, the lift was not enough to stop the unemployment rate from rising to the 4% handle.

Job openings, job quits, job hires, NFP

Source: Refinitiv, prepared by Richard Snow