S&P 500, Volatility, FTSE 100 and Hang Seng Fundamental Forecast Talking Points:

- Global equities have generally held steadfast or advanced through the opening week of the year, which is impressive given the still-troubled backdrop

- A favorable Fed rate forecast shift from the NFPs this past week didn’t seem to spill over to the S&P 500, nor did the ISM service sector plunge – will bank earnings change the calculus?

- Even more remarkable than the US indices is UK’s FTSE 100 which is eyeing record highs despite clear recession warnings and Hong Kong’s Heng Sang charging higher

Recommended by John Kicklighter

Get Your Free Equities Forecast

Fundamental Forecast for the S&P 500: Bearish

Globally, equities seem to be in a generally optimistic position. There may be some measure of seasonal influence at play in this stance or a lot of speculative appetite; but in many instances, it is increasingly conflicting with the tangible fundamental outlook. The IMF kicked off 2023 with a warning that a third of the world’s economies are facing a recession this year; and for many of those not in a technical contraction, it will feel like one. It is likely that the markets have become conditioned over the past decade to dismiss natural economic and financial troubles owing the outsized influence of the world’s central banks. Through much of recent history, these major institutions have stepped in with stimulus even when there wasn’t a tangible economic concern but merely the sign of a market tantrum. Yet, with the extraordinary inflation levels of the past year and risk of embedded higher prices for the future (it doesn’t have to be at the extremes); there is little chance that the authorities are still the reliable backstop they once were.

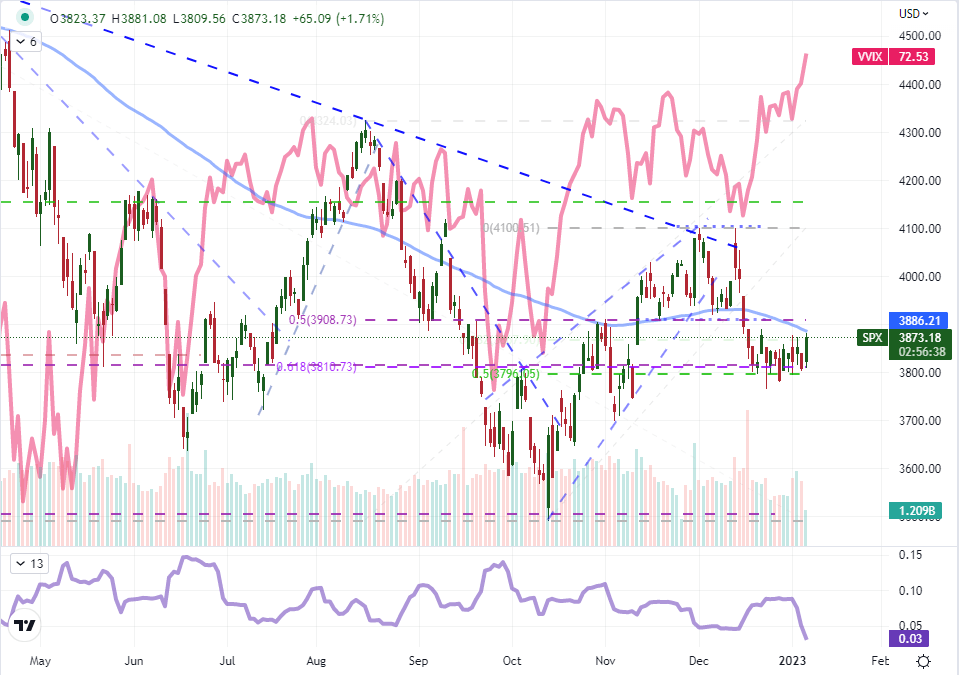

When it comes to setting expectations straight on what central banks will and will not do, there has been no more transparent a group than the Federal Reserve. They have reiterated their stance that rates in 2023 will peak at consensus of 5.1 percent and no cuts will be realized before year’s end. The market has constantly discounted that view. After the December employment report this past week, the rate forecast for June (the loose terminal time frame) ebbed with a notable boost for the S&P 500. What is far more remarkable though is that the slump in the ISM service sector survey (49.6) – which is a strong proxy for the broader economy – furthered the Friday bounce on a small change in rate forecasts. That is remarkable considering it significantly raises the onus of a recession and everything that means for the markets. Ultimately, this index is still carving out an extraordinarily narrow range as a carry over of seasonal conditions and is in the middle of its range. The Dow is near multi-month highs and the Nasdaq 100 on the verge of fresh multi-year lows. The common factor is the extremely low level of expected volatility. Below, I overlaid (an inverted) VVIX Index. This is a volatility of volatility measure that is a better measure of complacency than the standard VIX. It has pushed to lows not seen since March 2017. That is extreme and carries a meaningful directional influence.

of clients are net long. of clients are net short.

| Change in | Longs | Shorts | OI |

| Daily | -14% | 15% | -3% |

| Weekly | -8% | 7% | -1% |

Chart of S&P 500 Overlaid with Inverted VVIX Index, 14-Day Historical Range (Daily)

Chart Created on Tradingview Platform

Fundamental Forecast for the FTSE 100: Bearish

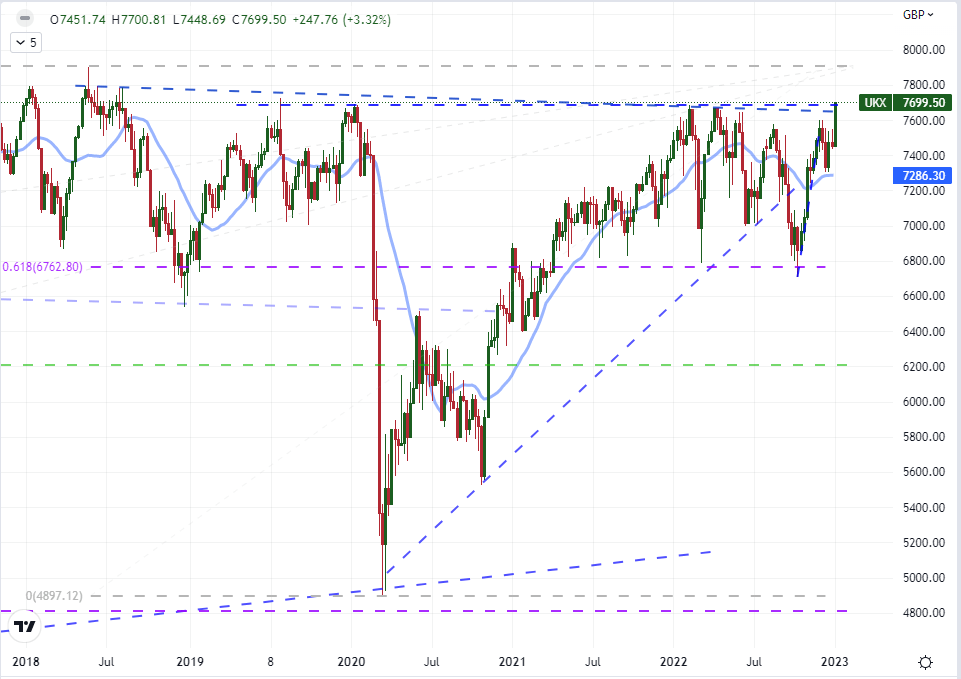

If the S&P 500’s resilience is remarkable, the UK-based FTSE 100’s standings are extraordinary. The 3.3 percent charge through the opening week of the year is impressive in its own right, but there wasn’t much in the way of scheduled fundamentals that would get in the way of a seasonal charge. What is more remarkable is where it has ended the week. It was the highest close since July 2018. Technicians will definitely be arguing whether this was a break or test of the multi-month range of highs, but the fundamentally-minded have to point out the backdrop circumstances for the economy. The Bank of England has not been shy about its warnings that the United Kingdom was facing a recession this year. It has said this in the context of reflecting on exceptional high inflation and reiterating that interest rates will need to remain high in order to keep price pressures from becoming sticky. No central bank help and economic struggle does not exactly scream support for the FSTE 100’s eying record highs. Perhaps general risk trends or key data (Friday’s run includes the monthly GDP report) will shake the bulls from their trance.

of clients are net long. of clients are net short.

| Change in | Longs | Shorts | OI |

| Daily | -11% | 2% | 1% |

| Weekly | -57% | 57% | 24% |

Chart of FTSE 100 (Weekly)

Chart Created on Tradingview Platform

Recommended by John Kicklighter

Improve your trading with IG Client Sentiment Data

Fundamental Forecast for the Hang Seng: Bullish

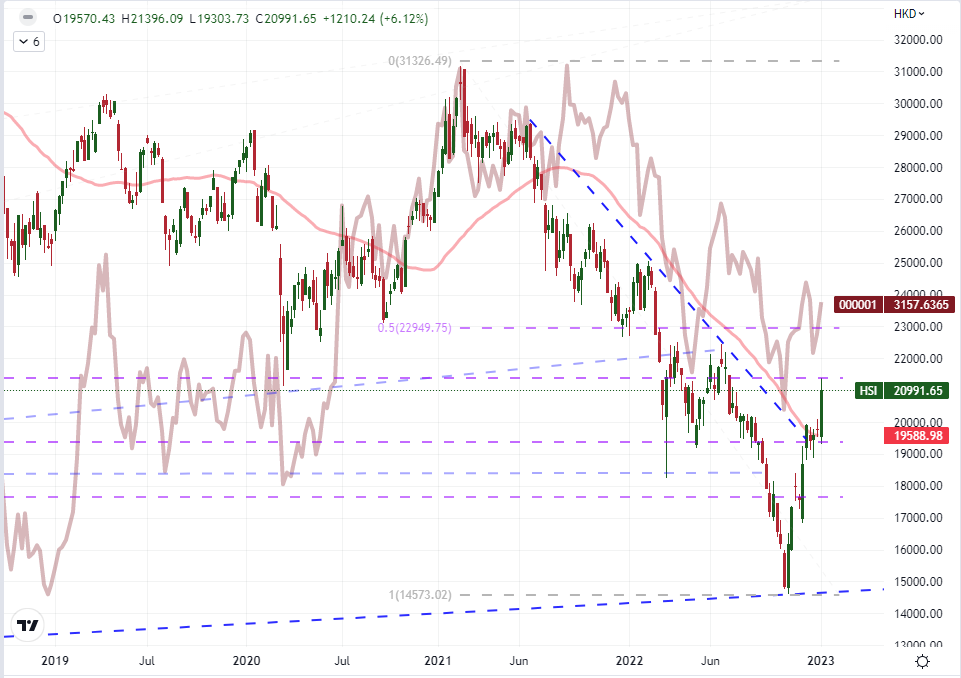

Where I maintain considerable skepticism around the confidence in many regions’ indices, one of the areas that I hold out the possibility for further improvement despite the global position is in China and its administrative regions. China – the world’s second largest economy – has registered a significant slump in economic activity that has been exacerbated by the strict Covid protocols of the past year. With the shift in stance around ‘Zero Covid’, the reopening of the economy has led to a surge in cases of illnesses but it has also drawn scrutiny to the impact this wave has on growth potential from an avoidance of shopping and absence of workers for production – even if the government will allow for it. It is likely that the spread of the virus will have a negative impact on the economy, but it is likely to be less severe an impact than would be full lockdowns given its impact on domestic consumption and supply chain constraints in a region already flooded with stimulus via high-yield lending. While this is a fundamental consideration for mainland, it also has its impact on the administrative regions. In particular, the flow of financing through Hong Kong stands to benefit the investment into a reopened economy. The Hang Seng earned a 6.2 percent rally this past week (the 5th such week of that magnitude or greater since the October bottom) and cleared its 200-day simple moving average.

Chart of Hang Seng Index Overlaid with Shanghai Composite (Weekly)

Chart Created on Tradingview Platform

Discover what kind of forex trader you are